ZIC Tax Highlights: Stamp Duty on Employment Contracts

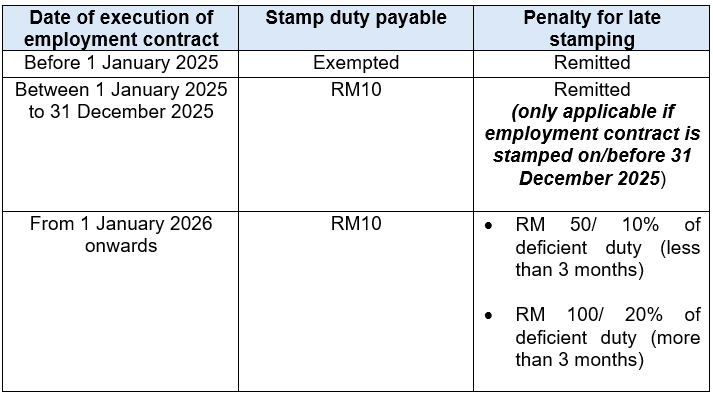

The Malaysian Inland Revenue Board (“IRB”) of Malaysia has recently picked up stricter enforcement on the Malaysian Stamp Duty Act 1949. In line with this, the IRB had initially commenced audit on various companies and required all employment contracts be subjected to stamping, and where applicable, late stamping penalty was imposed. Upon various lobbying efforts, the IRB issued an announcement to provide blanket remission on employment contracts, which can be summarized as follows:

Following this, a set of FAQs was issued by the IRB, [1] to provide further clarity on matters relating to imposition of stamp duty on employment contracts. Main takeaways are outlined below:

1. Who is responsible for paying stamp duty-employer or employee?

The person who signs the document first is responsible for paying stamp duty. Generally, it would be the employer.

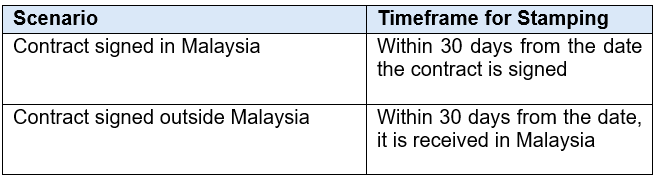

2. What is the timeframe for stamping an employment contract after it is signed?

An employment contract must be stamped within the following period:

3. Are temporary, short-term, part-time, or contract employment agreements required to be stamped?

Yes, all employment contracts have to be stamped.

4. Is stamping required each time an employment contract is renewed?

Yes, each new employment contract is treated as a separate instrument and must be stamped.

5. Is it necessary to submit employment contracts signed before 1 January 2025 to LHDNM for endorsement?

Employment contracts that have been granted an exemption may be submitted to IRB for assessment and endorsement in order to obtain a stamp duty exemption certificate.

6. Is there a fee for endorsing an exempted employment contract?

No fee is imposed unless the original stamp duty exceeds RM 10.

How Can We Help?

Considering the stricter enforcement of the Malaysian Stamp Act 1949 vis-a-vis increase in stamp duty audits and the impending stamp duty self-assessment system commencing 1 January 2026, our Tax & Duties team here at Zaid Ibrahim & Co. remains steadfast in assisting all taxpayers. Our legal assistance ranges from providing stamp duty trainings on the introduction and understanding the provisions of the Stamp Act and avoiding pitfalls, legal advice in applicable duties on instruments, to dispute work defending against stamp duty assessments be it by way of notice of objections or appeals to the Malaysian Courts.

[1] FAQ by Inland Revenue Board (3 July 2025) “Soalan Lazim 9FAQ) Penyeteman Kontrak Penggajian di Malaysia”